Condo Home Warranty: Coverage, HOA Considerations, and Real Costs

Condo home warranty focuses on the things inside your unit that you’re responsible for: HVAC components that serve only your space, in-unit plumbing and electrical, and everyday appliances. It steps in when covered items fail due to normal wear and tear. The warranty does not cover the building shell or shared systems, such as the roof, elevators, main risers, or a central boiler/chiller.

Think of it next to your HOA master policy and your HO-6 condo insurance. The master policy handles the building and common elements. HO-6 covers your finishes, personal property, and many types of sudden damage. The warranty pays for fixing the breakdown itself on covered items. The trio plays best when you match a plan to your building’s setup, get pre-approval before work starts, and budget for access work that many providers exclude.

How Condo Coverage Works (And Where It Stops)

A condo home warranty plan focuses on what’s inside your four walls, the systems and appliances that you personally maintain and control. It’s designed to keep life predictable when the essentials break down from normal wear and tear.

Most condo home warranty plan cover the key items that keep your home running day to day:

- Heating and cooling systems that serve only your unit (like fan-coil or PTAC units)

- Plumbing inside the unit, including supply lines, drain lines, and shut-off valves

- Electrical wiring, outlets, and panels located within the unit

- Kitchen and laundry appliances, from dishwashers to dryers

Anything that connects to a shared or building-wide system usually falls outside the plan’s boundaries. Once a pipe, duct, or wire leaves your unit and enters a common area, it typically becomes the HOA’s responsibility rather than yours.

There are a few common exclusions and limits that every condo owner should keep in mind:

- Pre-existing or known issues that existed before your coverage started

- Code upgrades or bringing old systems “up to standard”

- Access through shared walls or ceilings, which many providers won’t cover

- Secondary damage, like water stains or flooring repairs caused by a leak

Condo living adds its own set of quirks. Shared vertical plumbing stacks, ceiling chases, and fan-coil units can blur the lines between personal and shared responsibility. Some condos rely on building-supplied hot or chilled water, meaning the warranty covers your in-unit components but not the central system feeding them.

Understanding where your coverage begins and ends helps you avoid claim surprises and coordinate smoothly with your HOA or property manager. For more detail, see Understanding What’s Covered and What are exclusions.

HOA, Master Policy, and Your HO-6: Who Pays What?

Condo protection works as a three-part stack. The HOA master policy takes care of the building and shared elements. Your HO-6 condo insurance covers interior finishes, personal property, and many kinds of sudden damage. A home warranty handles covered breakdowns of the systems and appliances you maintain inside the unit. When something fails, start by identifying where the problem lives and who controls that component.

Decision flow you can follow

- Locate the component. Is it inside your unit and solely serving your space?

- Check control and maintenance. If you maintain it, a warranty claim may apply.

- Confirm building involvement. If the fix requires work in a common area or touches a shared system, expect HOA/master policy rules to steer the process.

- Document and open the right tickets. Warranty claim for the breakdown; HO-6 for interior damage; HOA work order for common elements.

- Get written pre-approval. Scope, coverage cap, and service fee in writing before any work.

Practical tips for smooth claims

- Keep photos, model/serials, and your claim number handy.

- Ask the property manager for approved vendor requirements and COI details before a tech arrives.

- Clarify access responsibilities. Many plans don’t pay to open and close shared walls or ceilings.

- Coordinate after-hours rules and elevator scheduling so a tech can reach your floor without delays.

Read here how home warranty is different from insurance.

Real-World Claim Scenarios in Condos

A condo warranty claim can feel tricky when systems are shared, walls are common, and responsibility lines blur. Here are a few everyday examples that show where coverage starts and where it stops.

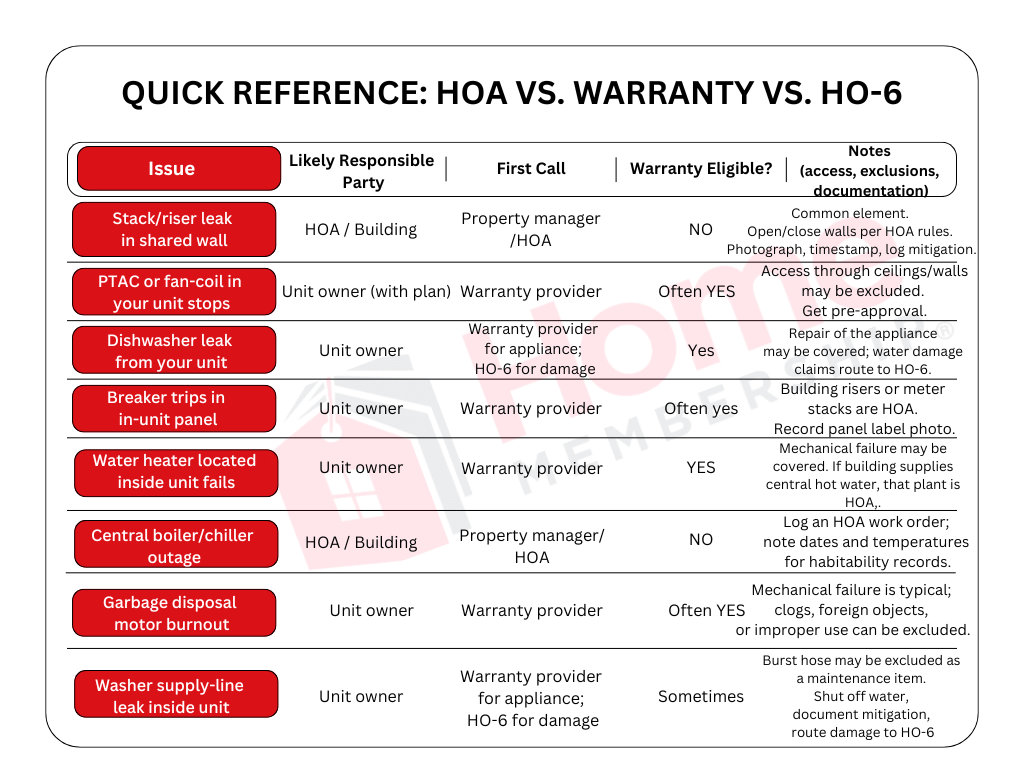

1. Stack Plumbing Leak

A vertical “stack” carries drain water through several units. If the leak is inside your unit’s own plumbing, your warranty may cover the repair after pre-approval. Once the damaged pipe sits behind a neighbor’s wall or in a shared chase, it becomes a common element managed by the HOA.

Before any wall is opened, check with the property manager. The HOA often must authorize access in shared areas and hire its own vendor for common piping. Your warranty provider won’t restore drywall, flooring, or paint unless your plan lists limited access coverage.

Tip: Always photograph the area, shut off the water, and log a warranty claim and an HOA report at the same time so both parties stay aligned.

Here you can understand what Home warranties Plumbing Coverage is.

2. Fan-Coil or PTAC Failure

In most condos, heating and cooling inside your unit rely on fan-coil units or PTACs (through-wall heat pumps). These belong to you and are usually covered for parts and labor when a motor, capacitor, or control board fails.

If the problem traces back to the building’s central chiller or boiler, that’s not your warranty item. Those large systems fall under the HOA’s master policy and maintenance schedule.

Tip: Describe symptoms carefully when opening a claim, “fan not blowing” keeps the focus on your unit’s equipment, while “no hot water from building loop” signals a shared system.

3. Electrical Panel vs. Common Risers

Your in-unit electrical panel, breakers, and outlets are part of your space, and most plans include them. The feed risers or meter stacks in a common chase belong to the building. If the issue sits between the main riser and your panel, it’s outside warranty territory and typically handled by the HOA’s electrician.

Tip: When lights flicker or power drops, check whether neighbors are affected. If multiple units lose power, call the property manager first, not your warranty provider.

4. Water Heater Confusion

If your condo has a tank or tankless water heater inside the unit, the warranty often covers mechanical failures like thermostat or element burnout. When hot water comes from a central boiler system, none of that equipment is yours to maintain, and warranty coverage stops at the supply connection inside your unit.

Tip: Snap a photo of your setup. Seeing the tank, shut-offs, and labeling helps confirm whether it’s an in-unit appliance or part of the building plant.

Each of these examples shows the same rule in action: a condo home warranty protects what you own and maintain inside your space. Once the problem crosses into shared infrastructure, the HOA’s master policy or your HO-6 insurance steps in. Clear communication with your property manager and warranty provider keeps every claim on track and avoids back-and-forth about who pays for what.

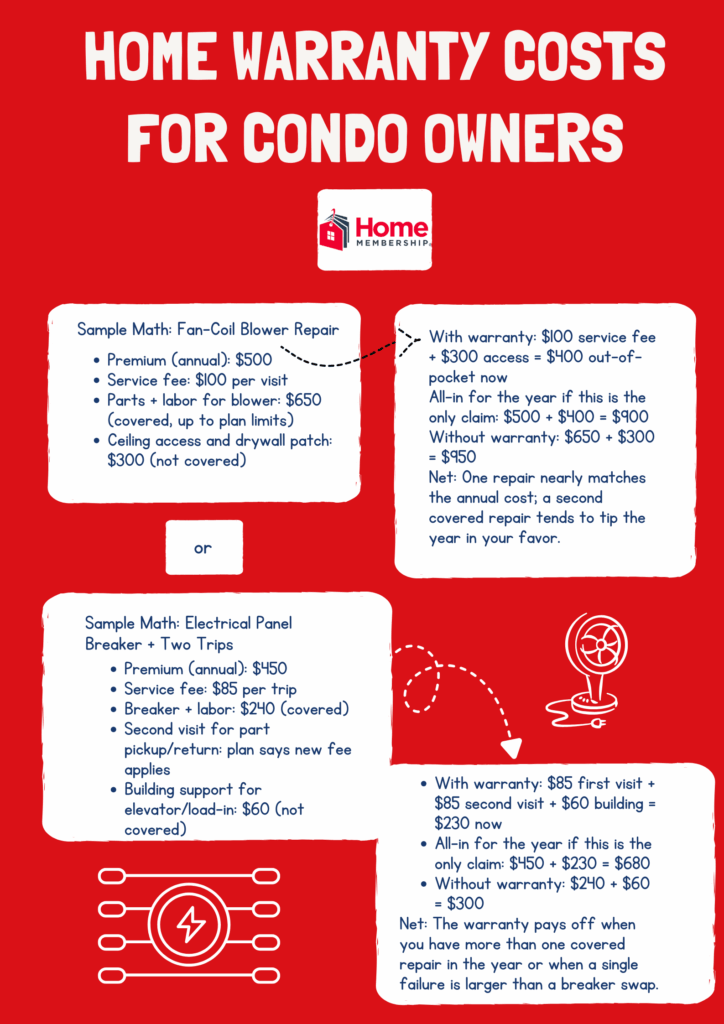

Home Warranty Costs for Condo Owners

Typical yearly premium: Most condo-sized plans land in the $400–$600 per year range. Condos tend to have fewer major components inside the unit than single-family homes, which helps keep premiums moderate. Pricing reflects the plan tier you pick and the reality that access can be harder in buildings.

Service fee per claim: Expect a fixed visit fee each time a contractor is dispatched. If a tech needs a second trip for parts, you may see a second fee unless your plan states one fee per repair. Read the trip-fee language closely so you can budget with confidence.

Access and labor in condos: Many providers limit or exclude costs tied to building logistics. Common owner or HOA expenses include:

- Ceiling or wall access to reach a shared chase

- Permits or building-required inspections

- Elevator scheduling, load-in, parking, and after-hours rules

- COI requirements or use of HOA-approved vendors

These items sit outside a typical warranty and get billed to the unit owner or the HOA per your building rules.

When a plan saves money vs. paying out-of-pocket:

- Your unit has aging in-unit equipment (fan-coil, PTAC, dishwasher, disposal, panel)

- You prefer predictable costs over surprise repair bills

- Your building setup increases the odds of multiple small-to-mid repairs in a year

To understand the costs and benefits from home warranty you’ll need to read about it.

Before You File: Condo-Specific Pre-Approval Steps

Condo claims move smoothly when you line up three things first: approval from your warranty provider, coordination with building management, and solid documentation. Taking these steps saves time, avoids denials, and keeps everyone on the same page.

1. Get Written Pre-Approval

Every claim should start with a formal authorization that lists the repair scope, coverage cap, and service fee. This document is your green light to begin work. If a tech starts before approval, the claim can be denied. Ask for confirmation by email or through your provider’s portal so there’s a record.

2. Coordinate with Your HOA or Property Manager

Condos often have strict building rules, and skipping them can delay your repair.

Check for:

- Required notice before a contractor arrives

- Approved vendor list (some HOAs only allow pre-screened trades)

- Certificate of Insurance (COI) requirements for any tech entering the building

- After-hours or elevator scheduling rules, which may add access fees not covered by your plan

Confirm these details early and share them with your warranty provider so they can schedule accordingly.

3. Document Everything

Before the tech arrives, take clear photos of model and serial numbers on the affected equipment. Keep your claim number, any emails or texts from the provider, and note the steps you took to prevent further damage, like shutting off water or protecting floors. Providers expect this basic mitigation.

A simple folder on your phone or desktop labeled “Home Warranty Claims” makes it easy to track invoices, approvals, and communication threads. These records help if coverage questions come up later.

For full guidance, see Reading Between the Lines of Home Warranty Contracts.

How to Choose a Condo-Friendly Plan

Finding the right condo home warranty isn’t about picking the cheapest premium. The best plan fits your building setup, your unit’s systems, and the rules your HOA enforces.

Start with the right questions

When you shop for coverage, dig into the details that matter most in a condo:

- Access coverage: Will the plan pay to open and close ceilings or walls if a tech needs to reach hidden lines?

- Multi-trip fees: Does the provider charge a new service fee if the technician has to return with parts?

- Building-supplied utilities: If heating or cooling water comes from a central plant, does the plan still cover your in-unit fan-coil or PTAC components?

- Fan-coil or mini-split systems: Are parts like blower motors and control boards listed as eligible items?

- Pipe leaks in shared chases: Does coverage end at your unit boundary, or will they help diagnose leaks that start just beyond it?

Asking these questions up front helps you avoid the fine-print surprises that often appear once a claim is filed.

Compare by fit, not just price

Condo coverage is about alignment, not just savings. Review your HOA’s maintenance chart and match each system to who’s responsible- you, the HOA, or a shared service. Then check if the plan’s list of covered items overlaps the systems you actually own and maintain.

A slightly higher premium can make sense if it includes tricky condo features such as ceiling access or multi-visit protection. Once you find a plan that mirrors your unit’s reality, the warranty works the way it’s meant to: predictable, clear, and hassle-free.

Here are 8 factors that you should consider when choosing home warranty.

The Bottom Line

A Condo home warranty makes sense when you want predictable repair costs for the systems and appliances you personally maintain inside your unit. They step in for breakdowns caused by wear and tear, which are the things your HOA master policy or HO-6 insurance won’t touch. The warranty won’t replace insurance or the HOA’s coverage, but it fills the gap between the two by taking care of your everyday mechanical and appliance issues.

If a repair involves shared systems or building-wide components, that’s when the HOA master policy comes into play. When a failure causes damage, such as water soaking floors or ceilings, your HO-6 insurance covers the restoration. The key is to match your warranty plan to your building’s structure and access rules. The clearer you understand who owns what, the fewer surprises you’ll have when a claim hits. A well-chosen home warranty plan saves money, time, and stress, especially in buildings where service calls require coordination and access approvals.

Related Posts