Ultimate Guide to The Cost of Home Ownership 2025

Understanding the cost of home ownership is essential, and buying a home is just the start. In 2025, plan for rising taxes, insurance, utilities, maintenance, and the occasional surprise repair. And remember the big picture: roughly a third of U.S. households are “cost-burdened,” spending ≥30% of income on housing, with wide state-by-state variation, according to a Statista analysis published June 27, 2025. The U.S. homeownership rate edged from 65.6% in 2024 to ~65.0% by Q2 2025, a change the Census says isn’t statistically significant.

This guide gives you a clear, line-by-line breakdown so you can budget with confidence.

TL;DR cost snapshot

First-year vs. ongoing

- First year: Expect the highest spend. Beyond the mortgage/escrow, you’ll likely pay for inspection punch-list fixes, small upgrades (locks, blinds, paint), basic tools, and catching up on deferred maintenance.

- Ongoing years: Costs stabilize once utilities, taxes, insurance, HOA, and routine upkeep settle in. Plan quarterly check-ins and bump the maintenance pot if a big system is aging.

How much to set aside

- Rule of thumb: save 1%–3% of home value per year for maintenance and wear-and-tear repairs.

- Newer/condo or small home: closer to 1%

Older/large single-family or harsh climate: 2%–3%

- Newer/condo or small home: closer to 1%

- Quick example: on a $350,000 home, budget $3,500–$10,500/year.

Optional risk management

- A home warranty can offset covered repair costs for major systems/appliances and smooth out surprise bills. Learn how to use it effectively in our Guide to Home Warranty.

What’s included in the true cost of owning a home

Understanding each expense helps you budget smartly and find places to save.

Mortgage (principal + interest)

Your main payment—principal builds equity, interest is borrowing cost. Even small rate changes can shift your monthly budget.

Property taxes

Based on your home’s assessed value and local rates. Expect changes after reassessment or upgrades.

Homeowners insurance

Protects your structure, belongings, and liability. Compare deductibles and exclusions; update coverage after renovations.

Mortgage insurance (if applicable)

PMI or MIP protects lenders when you put down less than 20%. Plan to remove it once you build enough equity.

Utilities

Electricity, water, gas, trash, and internet vary by season and efficiency. Smart upgrades like insulation and thermostats can cut costs.

HOA or condo fees

Cover shared areas and amenities. Review financial reserves to avoid surprise assessments.

Maintenance & reserves

Budget for upkeep and big-ticket replacements—roof, HVAC, or water heater. A home warranty can offset repair costs and reduce surprises.

Each of these factors adds up to the real cost of owning a home, so tracking them helps you plan ahead confidently.

2025 monthly & annual budget framework

Sample budget table (U.S. example)

| Cost Category | Monthly | Annual | Notes |

| Mortgage (P+I) | $2,395 | $28,741 | ~$360k loan @ ~7% for 30 years (illustrative). |

| Property taxes | $348 | $4,172 | U.S. average bill for single-family homes in 2024. The Title Report |

| HOI (homeowners insurance) | $176 | $2,110 | U.S. average premium (varies widely by state). |

| Mortgage insurance (PMI) | $120 | $1,440 | ~0.4% of loan amount (good-credit example). |

| Utilities (avg.) | $590 | $7,080 | Electric, gas, water/sewer, trash, internet/cable, typical bundle. |

| HOA/condo fees | $120 | $1,440 | 2024 U.S. median monthly fee for mortgaged households. Census.gov |

| Maintenance (1%–3%/yr) | $667 | $8,000 | Midpoint example (2% of $400k). Adjust by age/condition/climate. |

| Home warranty | $58 | $700 | Typical systems+appliances plan. Compare at /plans. |

| Total | $4,474 | $53,683 | First-year may run higher due to move-in fixes and tools. |

Assumptions & tips

- Swap in your actual rate/loan amount for the mortgage line. A 0.5% rate change can shift P+I by ~$120–$140/month in this example.

- For maintenance, use 1%–3% of home value (newer/condo ~1%; older/SFH in harsh climates ~2%–3%).

- If you carry <20% down, use your lender’s PMI quote; typical ranges vary by credit and LTV. NerdWallet

- Want to smooth repair surprises? Pair your maintenance reserve with a plan from /plans and review our Guide to Using Your Home Warranty for faster approvals and fewer denials.

Big 2025 factors shaping the cost of home ownership

Interest rates & refinancing math (quick scenarios)

30-yr vs. 15-yr (illustrative, $360k loan)

- 30-yr @ 7.00%: ≈ $2,395/mo P&I

- 15-yr @ 6.25%: ≈ $3,087/mo P&I

- Takeaway: 15-yr raises the payment but cuts total interest dramatically and builds equity faster. 30-yr keeps cash flow lighter.

Rate drops and savings

- 7.00% → 6.50% (30-yr): ≈ $120/mo savings (from ~$2,395 to ~$2,275).

- 7.00% → 5.75% (15-yr): payment rises (~$2,395 → ~$2,989) but you finish sooner and slash lifetime interest.

When a refi makes sense (breakeven check)

- Use: Breakeven months = Closing costs ÷ Monthly savings.

- Example: $4,000 costs ÷ $120 savings ≈ 33 months to breakeven.

- Green flags: You’ll stay past breakeven, your new APR is meaningfully lower (rule of thumb: ≥0.5–1.0% drop), and you’re not extending the term so far that it erases gains.

- Bonus wins: You can drop PMI, shorten the term, or consolidate a HELOC at a lower fixed rate.

Insurance shifts (weather & premiums)

Regional volatility (coastal, wildfire, hail belts)

- Carriers are tightening underwriting where risk is rising—coastal wind/flood, wildfire–urban interfaces, and hail/tornado corridors. Expect higher premiums, stricter inspections, roof-age limits, and in some ZIP codes, non-renewals. Get quotes early and compare wind/hail deductibles and required mitigation (roof type, defensible space, shutters).

Deductibles and coverage gaps to watch

- Wind/hail or hurricane percentage deductibles (e.g., 2% of dwelling limit) can dwarf flat deductibles.

- Excluded perils: flood and earthquake are typically separate policies.

- Actual Cash Value (ACV) vs. Replacement Cost on roofs and personal property changes your payout dramatically.

- Check ordinance or law coverage, water backup, service line, and loss-of-use limits—common weak spots.

Property taxes & assessments

Reassessment cycles, school levies, special assessments

- Many jurisdictions reassess on set cycles or at transfer—expect jumps after purchase or remodels.

- School levies/bonds and local improvements (streets, sewers) can add special assessments to the bill. Track local ballot measures and your county assessor’s calendar.

How improvements can change your tax bill

- Permitted upgrades (additions, finished basements, major kitchen/bath) can raise assessed value.

- Some energy/aging-in-place improvements may qualify for exemptions or abatements—ask your assessor before work begins.

- Verify homestead or primary residence status; missing it can cost you hundreds per year.

Utilities & efficiency

Energy price trends + what you can control

- You can’t set market rates, but you can shrink usage and peak demand. Focus on quick wins with clear payback:

- LED lighting: Low cost; often <1–2 year payback.

- Smart thermostat: Typical 1–3 year payback via better scheduling and setbacks.

- Air sealing & insulation (attic/attic hatch/ducts): Frequently 2–5 year payback; also improves comfort.

- HVAC tune-ups & filters: Keep systems efficient; avoid costly failures.

- Heat pump water heater / high-efficiency heat pump: Bigger ticket, but strong savings in many climates; check rebates.

- Appliance upgrades (Energy Star): Time purchases with end-of-life to avoid sunk-cost waste.

- Ask your utility about free home energy audits, time-of-use plans, and rebates—they can stack and shorten payback periods.

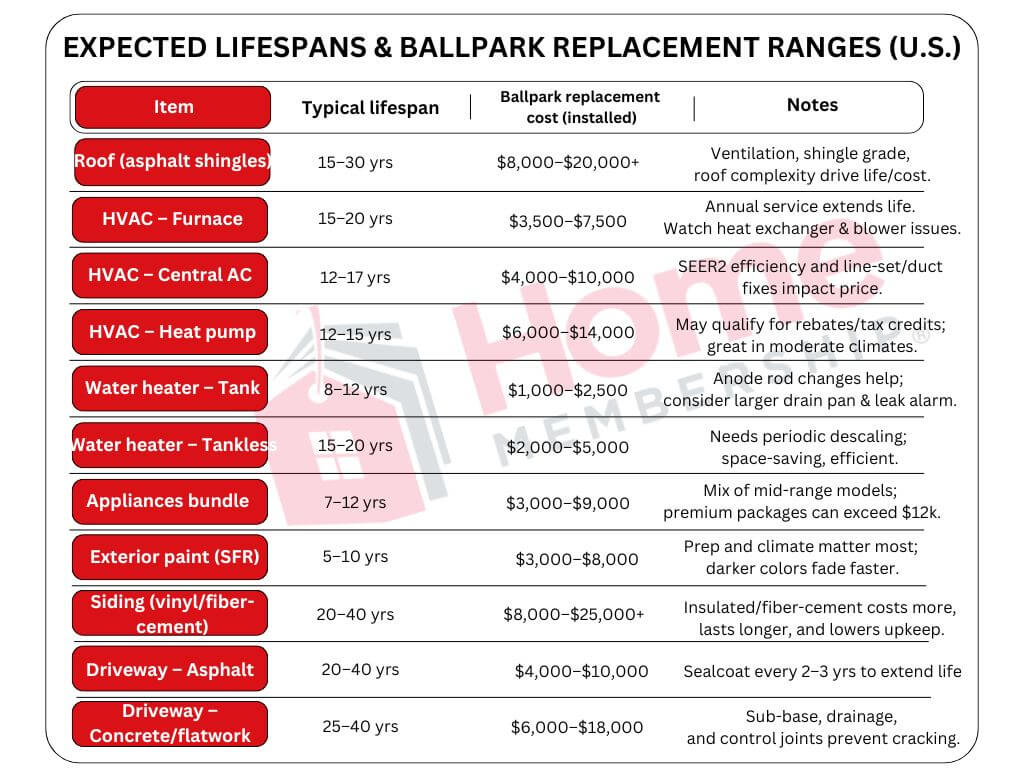

Maintenance & replacement: planning the big-ticket items

Budgeting for end-of-life items keeps surprises from wrecking your year. Use the ranges below as planning guides, these are actual costs vary by size, region, and spec.

Planning tips

- Add 10%–20% contingency for permits, disposal, code upgrades, or access issues.

- Prioritize items with active leaks or safety risks (roof, water heater, furnace heat exchanger).

- Routine upkeep—filter changes, caulking, gutter cleaning, paint touch-ups—can add years to lifespan.

CTA: Not every failure means full replacement—many issues are repairable and can be covered under a plan. Compare options at /plans.

Where a home warranty fits in your 2025 budget

What a home warranty typically covers

A plan helps pay to repair or replace major home systems (HVAC, electrical, plumbing, water heater) and appliances (fridge, range, dishwasher, washer/dryer) when they fail from normal wear and tear. It doesn’t replace homeowners insurance; it’s for breakdowns—not fire, flood, or theft.

Home warranty vs. emergency fund (they work together)

- Emergency fund = cash for anything (roof leak, ER visit, lost income). Flexible but finite.

- Home warranty = targeted protection for covered systems/appliances, with pre-set costs (premium + service fee).

- Smart setup: keep your emergency fund intact for non-covered events while the plan absorbs many repair bills you would have paid out-of-pocket.

Typical costs & how the math works

- Premium: usually $500–$900/yr for a systems + appliances plan.

- Service fee (per trade call): typically $75–$150 when a tech is dispatched.

- Quick example: Premium $750/yr + two covered repairs (A/C capacitor + dishwasher pump) with $100 service fee each = $750 + $200 = $950 total. Without a plan, those two repairs might run $1,100–$1,600, so you save and, more importantly, cap your risk.

Typical costs & how the math works (HomeMembership)

- Premium: commonly $300–$600/yr for a home warranty (general range noted on HomeMembership).

- Service fee (per trade call): $25.

When warranties deliver the most value

- Older equipment or mixed-age homes (A/C at year 12, water heater at year 9).

- High-labor markets where hourly rates inflate repair bills.

- Long parts lead times—having a plan helps coordinate approvals and source parts faster.

- Busy owners/landlords who prefer one call for qualified pros and predictable costs.

How HomeMembership does it

- Use trusted local techs: with our approach, you can work with qualified local pros (no mystery vendors).

- Clear, documented approvals: we guide you to open the claim first, get written pre-approval (scope + cap + service fee), then schedule work—reducing denials and delays.

- Transparent coverage by property type: start with See HomeMembership plans & pricing and choose the fit for single-family, condo, or townhome. Learn what’s covered & what isn’t so you know exactly how the process works before something breaks.

First-year costs vs. steady-state costs

Why year one is pricier

- One-time buys: inspection follow-ups, urgent fixes, basic tools, window coverings, new locks/rekeys, small furniture, safety gear (CO/smoke alarms, fire extinguisher).

- Move-in surprises: older appliances or HVAC can fail once they’re used hard (laundry catch-up, continuous A/C, full-family cooking). Budget a cushion for at least one unexpected repair.

How things settle by year two

- Recurring lines (mortgage/escrow, utilities, HOA, insurance) stabilize; you’ve handled most punch-list items.

- Shift from “set-up spending” to routine maintenance + reserves (1%–3%/yr of home value).

- Review insurance, shop utilities, and calibrate your maintenance reserve after 12 months of actual bills to lock in your steady-state budget.

Regional and property-type variations (quick matrix)

Why it matters: Ownership costs swing based on what you own and where you live—HOA rules, master policies, weather risks, and local labor rates all change the math.

By property type

| Property type | Cost drivers | What to watch |

| Single-family | Full responsibility for exterior + systems | Roof/driveway reserves, higher maintenance % (2%–3%) |

| Condo | HOA covers exterior/common areas; you cover in-unit | Master policy deductibles, special assessments, in-unit systems- see Condo Home Warranties |

| Townhome | Mix of condo/SFR responsibilities | Clarify HOA vs. owner scope for roof/siding- see Townhouse Home Warranties |

| Duplex/Tri/Quad | Multiple kitchens/systems; tenant wear | Higher maintenance, faster appliance turnover- see Multi-Family Unit Home Warranties |

By region

| Region | Cost drivers | What to watch |

| Coastal | Wind/hurricane, flood risk | Wind/hail % deductibles, separate flood policy, roof age |

| Snowbelt | Freeze/thaw, heavy heating loads | Roof/ice damming, HVAC/boiler service, higher winter utilities |

| Sunbelt | Cooling demand, sun exposure | HVAC lifespan, electric bills, exterior paint/UV wear |

| Hail/Tornado alley | Roof/siding damage frequency | Roof material/ratings, HOI deductibles, claim history |

| Wildfire zones | Insurability/defensible space | Premium volatility, non-renewals, mitigation requirements |

Quick tip: Adjust your maintenance reserve toward the higher end (2%–3%) for single-family homes in harsh climates or older buildings, and review HOA reserves/assessments before you buy.

Common mistakes that inflate ownership costs

- Under-budgeting maintenance; ignoring aging systems

Setting aside too little (or nothing) leads to bigger, rush-priced repairs later. Use 1%–3% of home value per year and increase toward 3% for older homes or harsh climates. - Starting work without written approval (claims get denied)

For warranty-covered items, open the claim first, get written pre-approval (scope + cap + service fee), then schedule work. - Skipping annual re-shopping of insurance and HOA addenda

Rates, deductibles, and exclusions change. Re-shop homeowners insurance yearly and review HOA master policy addenda so your in-unit coverage and deductibles align. - Not documenting serial numbers/photos for claims

Missing model/serials slows or sinks approvals. Keep a simple home inventory: photos of labels, installation dates, and receipts stored in a shared folder for fast claims.

Bottom line for 2025

The cost of home ownership is not just a mortgage; there are also taxes, insurance, utilities, routine upkeep, and eventual replacements. Build a total-cost mindset: set aside 1%–3% of home value for maintenance, map big-ticket lifespans (roof, HVAC, water heater), and review insurance, taxes, and HOA items annually. Use risk transfer where it makes sense, then a home warranty can smooth repair spikes and protect cash flow, while your emergency fund covers the rest.

Next steps

- Read here about Interactive Tools to Help Crunch Numbers and Simplify Choices

- Control repair risk: Compare HomeMembership plans & pricing and pick the coverage level that fits your home and budget.

Related Posts